Introduction

Auto insurance is one of the most important financial protections a vehicle owner can have. In most states across the United States, carrying at least a minimum level of auto insurance is legally required. However, many drivers purchase insurance without fully understanding what their policy covers or how different types of coverage can protect them financially after an accident.

Choosing the right auto insurance policy involves more than finding the lowest premium. The coverage you select can affect your financial security, repair costs, medical expenses, and liability in the event of an accident. With rising vehicle repair costs, increasing medical expenses, and growing traffic congestion, understanding insurance options has become more important than ever. Whether you’re buying your first policy or reviewing your current coverage, knowing how different insurance types work can help you make informed decisions and avoid costly mistakes. This guide explains the most common auto insurance coverage options available in the United States and how they can benefit drivers.

Why Auto Insurance Is Important

Auto insurance serves as a financial safety net when unexpected events occur.

Protects Against Financial Loss

Accidents can result in expensive vehicle repairs, medical bills, and legal claims.

Helps Meet Legal Requirements

Most states require drivers to carry certain minimum levels of insurance coverage.

Provides Peace of Mind

Knowing you’re protected can reduce stress and uncertainty while driving.

Understanding Basic Auto Insurance Coverage

Auto insurance policies often consist of multiple coverage types that work together to provide protection.

Not All Policies Are the Same

Coverage requirements and available options vary by state, insurer, and individual needs.

Choosing Appropriate Coverage Matters

A policy with insufficient coverage may leave drivers responsible for significant out-of-pocket expenses.

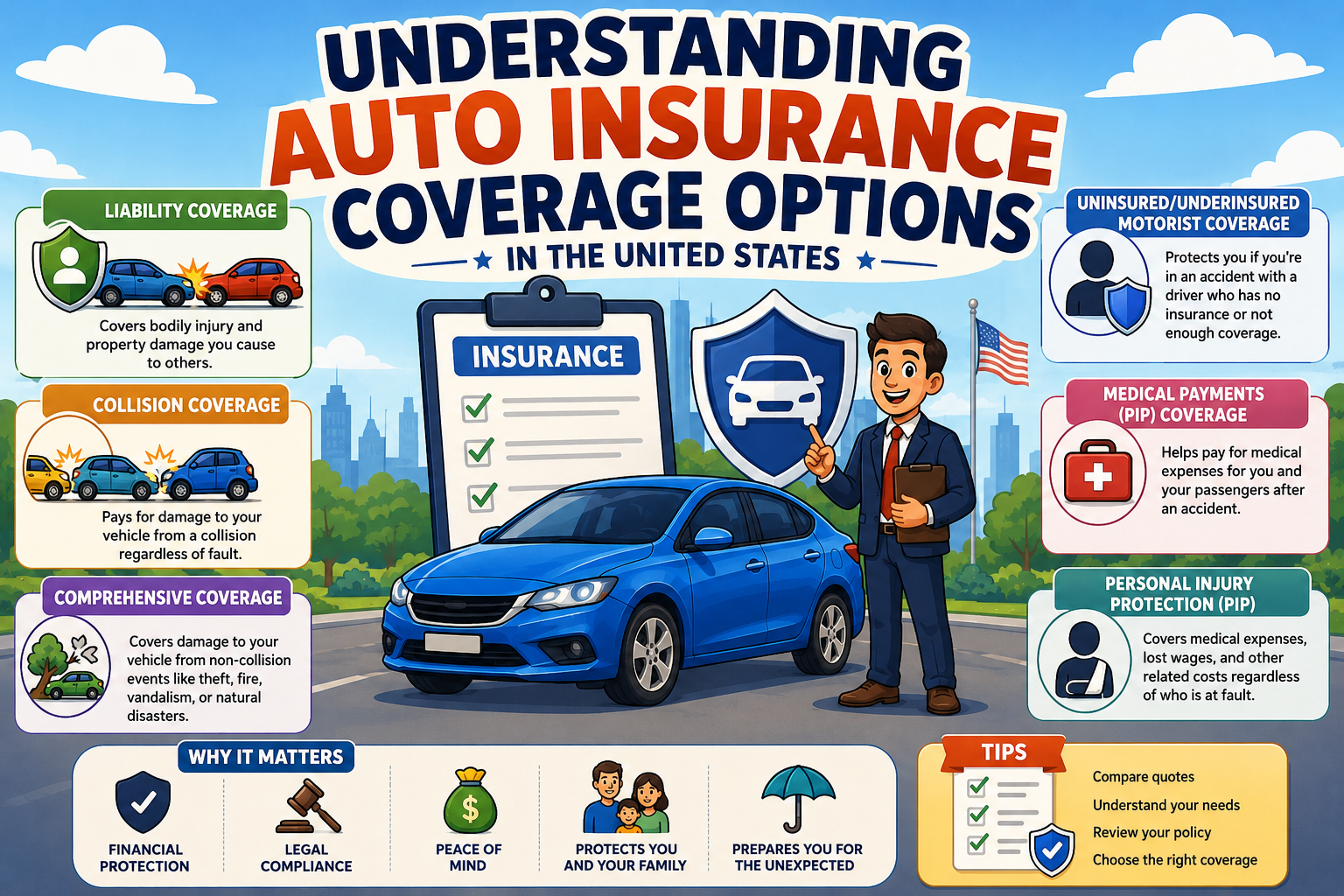

Liability Insurance Coverage

Liability insurance is the foundation of most auto insurance policies.

What Liability Insurance Covers

This coverage helps pay for damages and injuries you cause to others in an accident.

Bodily Injury Liability

Bodily injury liability may help cover:

- Medical expenses

- Lost wages

- Rehabilitation costs

- Legal expenses

for injured parties.

Property Damage Liability

Property damage liability typically covers:

- Vehicle repairs

- Building damage

- Fence repairs

- Other damaged property

Why It Is Important

Liability coverage helps protect your assets if you’re found responsible for an accident.

Collision Coverage

Collision coverage protects your own vehicle.

What Collision Insurance Covers

It generally helps pay for repairs or replacement if your vehicle is damaged in:

- Vehicle collisions

- Single-car accidents

- Accidents involving objects such as poles or guardrails

When Collision Coverage Is Valuable

Drivers with newer or higher-value vehicles often choose collision coverage to reduce potential repair expenses.

Comprehensive Coverage

Comprehensive coverage protects against non-collision-related damage.

Common Covered Events

Examples may include:

- Theft

- Vandalism

- Fire

- Falling objects

- Severe weather

- Animal collisions

Why Many Drivers Choose It

Comprehensive coverage provides protection against a wide range of unexpected situations beyond traditional accidents.

Uninsured Motorist Coverage

Unfortunately, not every driver on the road carries adequate insurance.

What Uninsured Motorist Coverage Does

This coverage may help pay for expenses if you’re involved in an accident caused by a driver who lacks insurance.

Potential Benefits

Coverage may help with:

- Medical bills

- Lost income

- Certain vehicle-related costs

Additional Protection

Some states require or strongly encourage uninsured motorist coverage due to the number of uninsured drivers on the road.

Underinsured Motorist Coverage

Even insured drivers may not always have enough coverage.

How It Works

Underinsured motorist coverage may help when the at-fault driver’s policy limits are insufficient to cover damages.

Why It Matters

Serious accidents can generate expenses that exceed minimum insurance requirements.

Additional protection can help reduce financial risk.

Personal Injury Protection (PIP)

Personal Injury Protection is available in certain states.

What PIP Covers

This coverage may help pay for:

- Medical treatment

- Rehabilitation

- Lost wages

- Essential services

regardless of who caused the accident.

Common in No-Fault States

Many no-fault insurance states require or offer Personal Injury Protection coverage.

Medical Payments Coverage

Medical Payments Coverage is sometimes called MedPay.

Purpose of MedPay

It helps cover medical expenses for:

- Drivers

- Passengers

- Family members in the vehicle

Coverage Examples

Benefits may apply to:

- Hospital visits

- Doctor appointments

- Emergency treatment

- Ambulance services

Medical Payments Coverage can provide valuable support after an accident.

Gap Insurance

Gap insurance is particularly relevant for financed or leased vehicles.

What Is Gap Insurance?

A vehicle may depreciate faster than the balance owed on a loan.

Gap insurance helps cover the difference between:

- The vehicle’s actual cash value

- The remaining loan balance

Who Should Consider It?

Drivers with new vehicles or low down payments often evaluate gap coverage as part of their insurance strategy.

Rental Reimbursement Coverage

Being without a vehicle after an accident can create challenges.

What It Covers

Rental reimbursement coverage may help pay for temporary transportation while your vehicle is being repaired after a covered claim.

Convenience Benefits

This coverage can reduce disruption to work, school, and daily activities.

Roadside Assistance Coverage

Many insurers offer optional roadside assistance programs.

Common Services Include

- Towing

- Battery jump-starts

- Flat tire assistance

- Lockout services

- Fuel delivery

Helpful for Emergencies

Roadside assistance can provide peace of mind, particularly for drivers who travel frequently.

Factors That Affect Insurance Premiums

Insurance costs vary significantly between drivers.

Driving History

Drivers with clean records often qualify for lower premiums.

Vehicle Type

Insurance costs may be influenced by:

- Vehicle value

- Repair costs

- Theft rates

- Safety features

Location

Urban areas often experience higher premiums due to increased accident frequency and vehicle theft rates.

Age and Experience

Younger and less experienced drivers typically face higher insurance costs.

Choosing Coverage Limits

Selecting the right limits is an important part of insurance planning.

Minimum Coverage vs Higher Limits

State minimum requirements may not provide sufficient protection in serious accidents.

Protecting Personal Assets

Higher liability limits can help protect savings, investments, and future earnings.

Evaluate Personal Risk

Coverage needs vary based on financial circumstances and individual comfort levels.

Ways to Lower Auto Insurance Costs

Insurance doesn’t have to be unnecessarily expensive.

Compare Multiple Quotes

Shopping around often helps drivers find better pricing.

Maintain a Clean Driving Record

Safe driving habits may result in lower premiums over time.

Bundle Insurance Policies

Many insurers offer discounts when multiple policies are purchased together.

Increase Deductibles Carefully

Higher deductibles can reduce premiums but may increase out-of-pocket costs after a claim.

Common Auto Insurance Mistakes

Choosing Coverage Based Only on Price

The cheapest policy isn’t always the best value.

Ignoring Policy Details

Understanding exclusions and limitations is essential.

Carrying Too Little Coverage

Minimum coverage may leave drivers financially vulnerable after serious accidents.

Failing to Review Policies Regularly

Insurance needs often change as vehicles, finances, and lifestyles evolve.

Recent Trends in Auto Insurance

The insurance industry continues to evolve.

Rising Repair Costs

Modern vehicles contain advanced technology that can increase repair expenses.

Increased Use of Telematics

Some insurers now offer usage-based insurance programs that monitor driving habits.

More Personalized Policies

Technology is allowing insurers to offer more customized coverage options.

Conclusion

Understanding auto insurance coverage options is essential for every driver in the United States. While liability insurance provides a foundation of protection, additional coverages such as collision, comprehensive, uninsured motorist, medical payments, and roadside assistance can offer valuable financial security when unexpected events occur.

The right insurance policy depends on your vehicle, budget, driving habits, and personal risk tolerance. Rather than focusing solely on finding the lowest premium, drivers should evaluate coverage limits, policy benefits, and long-term protection. By understanding how different coverage options work and reviewing policies regularly, motorists can make informed decisions that help protect both their vehicles and their financial well-being. A well-designed insurance policy offers more than legal compliance—it provides confidence and peace of mind every time you get behind the wheel.